Online Spins Bergen Casinos 2023 - When a casino offers bonuses for their games, they can be easily manipulated through the usage of multiple accounts, costing a lot of money for the gambling house.

Norwegian Deposit Card Games: Recently, most of the casino NetEnt has incorporated branded pokies on their list.

Theres plenty for nature lovers too a Butterfly Park which is home to 2,500 live butterflies from over 50 species and a Nature Walk that leads through lush jungle to the summit of Mount Imbiah, from where Singapores neighboring islands can be seen.

From the examples, the risks of the Martingale system should be clear, and the chief problem is that you can spend a lot of money, and you can spend it quickly.

Recently I’ve been reading “The General Theory of Employment, Interest, and Money” by John Maynard Keynes. There are few economists that really understand the way markets work, and human society functions. Classical economists, and monetary theorists, have built up an internally consistent logical framework for approaching the economy. However, this entire field of thought is wrong. Frankly, it does not matter if you THINK your understanding of the economy is correct, because it’s nice, elegant, and “logically” consistent. What matters is reality.

The economy is an emergent phenomenon. It does not arise out of any centrally planned office. It is haphazard and random. What the economy IS, is a measurement of how people choose to interact with each other. The economy represents relationships between people. Therefore, as it’s oft forgotten, the only thing that matters in the economy is people. The way people choose to interact. The way people re-act to news and events. The way people choose to structure their affairs. This is the only thing one should consider when attempting to understand the economy.

Relating this back to Keynes, in the general theory, Keynes begins by remarking on the postulates of employment laid out in classical economics. Classical economics states that workers should resist cuts in “real terms” but be unconcerned about cuts in “nominal terms”. However, this is not how people react. People are very very sensitive to changes in their nominal wages, and unless inflation is extremely high, will not really consider changes in real wages. Although, I’ve just started the General Theory, this initial salvo by Keynes against the classical theory, illustrates why I hold classical economics in such low regard.

The only real economic philosophy is Behavioral Economics. Understanding the psychology, neuro-biology, and sociological on-goings of the masses, is the only way to correctly understand the economy. In this vein, I see one true lineage of economic thought that begins with the mushy Adam Smith and his “Theory of Moral Sentiments” continuing with Keynes and his “General Theory” and finally Robert Shiller with “Irrational Exuberance”. This lineage more precisely understands the real economy, and the way reality actually works. Classical economists make books that sound nice. They seem elegant. But for all of their sophistication they fail miserably at understanding the way real people live their real lives.

Anyways, I’m not much of an economist, I just enjoy reading economic theory and understanding financial markets. The reason I mention Keynes and his general theory, is because of the novel insights he gives into how inflation should effect equities. With the understanding that at some level of inflation employees will not see raises, but there will be an increase in the price of goods, we should expect margins to increase. This is especially true where the primary input cost is labor. Thus, when you’re concerned your purchasing power is declining, keep your money in equities. Companies margins will increase, and therefore net income goes up, and if price-earnings remains the same, the asset price goes up! Thus, inflation is quite good for stocks, and should encourage you to purchase more when you see that CPI (consumer price index) going up!

Per my last post, I liquidated my position in Jinko Solar at around $60 a share, however had to realize a loss on the covered call I had sold, in order to do so. Following this liquidation I began buying shares of Carrier global at around $49.00 a share. However, since I no longer wanted Robinhood as my brokerage, but rather Wells Fargo, for reasons I shall delineate in a future article, I was forced to sell these shares at cost. Resettling the funds in my Wells Fargo account tied up my capital for approximately a week, during which time Carrier began trading at $51.50 a share, which represents my new cost basis. Hoping for a slight decline in price, I only purchased shares with ~80% of my portfolio allowing myself some flexibility to purchase shares should they decline slightly. Additionally, since I was unable to purchase option contracts on my new account, I could not leverage my belief in Carrier. Nonetheless, I believe my investment thesis in Carrier to be sound, and will delineate the reasons below.

I became interested in the prospect of HVAC (Heating, ventilation, and air conditioning) companies after reading an article in the New York Times. The article, titled, “Air-Conditioning Was Once Taboo in Seattle. Not Anymore”, made a compelling case for growth in the HVAC market. Further research yielded the largest HVAC companies, listed below by current market capitalization.

Daikin Industries ~ 60 Billion market cap (41 Price/Earnings TTM)

Carrier Global ~ 48.1 Billion market cap (21 Price/Earnings TTM)

Ingersoll RandInc ~ 20.5 Billion market cap (63 Price/Earnings TTM)

Not only was Carrier previously known to me, it also represented the cheapest large HVAC company. In a brief aside, Carrier was founded by Willis Carrier, who invented Air Conditioning. Additionally, Willis Carrier is an alum of Cornell University, where I’ll be attending this Fall! Recognizing the brand cachet I already associated with Carrier, I decided that it warranted a serious look as an investment.

Carrier Global, in its current iteration as a corporation, became public in 2020 following a spin off from United Technologies. This split created three separate companies, Raytheon Technologies (a defense manufacturer), Otis Worldwide (Elevator Manufacturer), and Carrier Global. Carrier’s portfolio focuses on three business segments: HVAC, Refrigeration, and Fire & Security. These three segments accounted for 53%, 19%, and 28%, respectively of the company’s $17.5 billion net sales in 2020.

This being only my first article on Carrier, and my need to mine content, I’ll only begin with a rough analysis of the HVAC segment. The HVAC segment will grow by both virtue of climate change, and Carrier’s strong brand recognition. Furthermore, Carrier has strong relationships with builders in key markets. This stickiness will translate to more sales as building and physical infrastructure ramps up over the next few years. Although demand for commercial and light commercial units may be depressed for the next few years, it will be more than offset by growth in the residential space. Given the extraordinary appreciation of home values over the last year, ~17% nationally, supply will certainly be trying to catch up and this can already be seen with housing starts, in June, up 29% year-over-year.

Also, Carrier is deploying a digital offering called Abound, which I believe will tie more real-estate developers to the Carrier ecosystem. The premise of the offering is to capture data about the air quality in commercial real estate and allow end users, consumers, to determine how safe a given building is. This is currently being marketed with Covid-19 in mind, however, I believe that this could easily be re-positioned from a pollution perspective. Densely populated regions such as New York or Deli, suffer from poor air quality that has serious adverse health consequences. In places such as these I believe end users will be very interested in the quality of the air they breathe. With the Abound pilot going well, I believe this offering, sold as a saas (software as a service) product, will further build the Carrier ecosystem and offer much higher margins than other products.

The reasons listed above are only some of the strengths I believe Carrier possess, and I will continue to expound on my investment thesis in future articles. Even with the rapid appreciation in price over the last week, I still believe that Carrier is priced cheaply and represents a very fair investment in the current market environment.

When I began purchasing Jinko Solar its share price was around $15 a share. Since then it has quadrupled in value than fell by half and is now trading at $60 a share. Recently, on June 25, Jinko Solar announced Q1 earnings. Their earnings while beating estimates led me to reevaluate the company’s fundamentals. The first major issue I have with the company is the huge disparity between EPS and diluted earnings. The diluted earnings per ADS (American Depository Share) and basic, respectively, was -$.55 and $.71. This disparity >100% means that Jinko Solar is likely to continue dilute any interest. Although this may make operational sense given Jinko Solar requires substantial capital to expand production capacity, I believe it illustrates the lack of responsibility management feels towards common shareholders.

$15.70 represents my initial entry $61.78 will likely be my selling point

Furthermore, rereading the company’s annual report illustrates substantial shortcomings. Firstly, the corporate structure of the company warrants serious scrutiny. The primary operating subsidiary of Jinko Solar limited is Jiangxi Jinko. Presently, Jinko Solar limited, the holding company JKS represents owns, ~75% of the operating subsidiary. This ownership will be further diminished with the STAR listing of another ~20%. While this capital infusion will be utilized to finance production capacity it is concerning how little Jinko, JKS actually represents. The STAR listing has led to a rapid appreciation of the ADS because the overly enthusiastic domestic Chinese markets will give a too optimistic valuation to Jinko’s common shares. Also, STAR listings do not have restraints on the maximum PE or profitability levels the traditional Chinese exchanges require. However, I do not believe Jinko Solar represents an operationally sound investment for the foreseeable future.

Although the solar industry seems poised for growth, Jinko Solar has seen continued pressure on their gross margins. While, I believe they will successfully expand into more premium products, the corporate structure is simply too complicated for me to be a continued investor. The company forms regional subsidiaries to manage certain operations and then turns over large portions of the equity? This practice seems exceedingly odd. I believe this structure may allow them obscure liabilities? or simply be poor management.

I sold call options at a strike price of $60 that expires August 20th. I expect these shares to be called away by then and any remaining shares I posses will be disposed of at $70. I believe the current price of Jinko Solar represents a fair price and any continued appreciation is speculation on the domestic demand for the new listing. Given that the ADS is not convertible for ordinary shares, this is actually not rational, although I suppose further equity could always be sold by the company at these lofty valuations.

The real mistake with my investment in Jinko Solar was not recognizing how expensive the shares had become at $90 previously. While this represented the optimism of a few incredible quarters, it did not consider the damaging corporate structure or the narrow financial edge that Jinko operates on. Furthermore, this price was achievable because certain senior convertible notes had not been exchanged for equity yet as to not dilute the share price. Any who, I believe going forward a clear price target, that represents fair value of a company, to me, should always be present in my mind. This way I know I should dispose of my shares in a company if they achieve fair value. this will prevent me from excoriating losses like I experienced earlier this year.

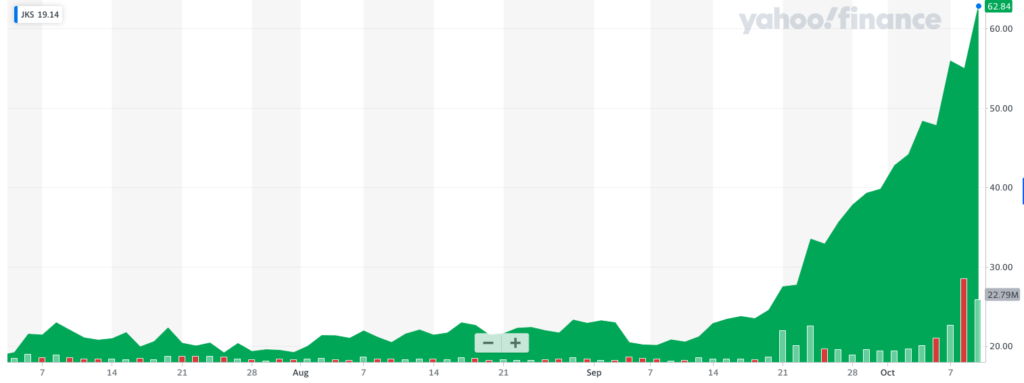

There has been a massive run up in Jinko’s shares recently. Since my initial article on Jinko Solar, the shares have increased 300%. Such a dramatic increase warrants a renewed look at the underlying company. Until I embark on a more thorough analysis of the company, I will leave a chart beginning with the date of my last update on JKS and ending at the most recent closing price.

Jinko Solar is the largest solar panel manufacturing by GW of panels deployed and sold annually. As more central governments develop stimulus programs an increasing caveat of these programs is a focus on clean energy. The rapidly declining price of solar makes it a viable alternative to traditional energy sources. However, what makes solar energy attractive for adoption is also a reason not to invest in it. Solar Panel manufacturing will likely go the way of P/C and become a commoditized product will low profit margins. Given that profit margins will inevitably decline substantially why do I believe in the company. Firstly, I believe there will be a significant increase in demand for solar panels given these new stimulus programs and policy changes. This will probably lead to increasing profits even with a decline in margins. Secondly, I believe the additional capital focused on environmentally conscious companies will lead to a valuation expansion for Jinko Solar. This should lead to a decent return in the intermediate term. The fact that I’ve bought into JKS American depository receipt and the passage of the “Holding Foreign Companies Accountable Act” will dampen this valuation expansion for the next few months until the bill is truly dead (or passed in which case the share price will suffer). Thirdly, Jinko Solar is already the largest solar panel manufacturing and with the economy in extreme distress smaller manufacturing firms will go out of business. This will increase the dominance of the larger players such as Jinko. While I believe this company will outperform in the intermediate term, once their primary product becomes commoditized margins will drop and handsome returns will be impossible, however until that occurs the company should perform fantastically.

The divergence between the economy and capital markets has only grown since the Coronavirus pandemic. With interest rates on bonds so low stocks seem to be the last place for reasonable growth. Amazon issued $10 billion in debt recently with an interest rate of .4%. When private companies can borrow at the same rate as the Federal Reserve, the debt market really has nowhere to go. As more capital leaves the debt market and makes a home in equities, prices will continue to rise. The rise in stocks is not necessarily rooted in optimism but in the reality of probable returns.

The senate unanimously passed this act yesterday. It’s amazing to believe the most polarized poltical body in the United States could agree to something so wholeheartedly. This amendment will have a material impact on the ADS (american depository securities) of foreign companies specifically Chinese companies. The major requirements of the bill are two fold

The PCAOB must be able to regulate the company in subject’s auditor

The Company must demonstrate that they are not owned by a central government

While many companies will be able to adhere to the first stipulation the bill was designed to exclude all Chinese companies from adhering to the second requirement. Considering the only position I currently possess is a Chinese security what does this mean for me.

Firstly, institutional investors will liquidate their equity shares in Chinese companies as a precautionary reaction to this bill. This will inevitably depress the share price of these companies significantly. Secondly, the uncertainty around the passage of this bill will lead to an immediate devaluation by the financial community of any Chinese security and will persist for sometime until the political reality becomes clear. Both of these reactions do not bode well for the short term performance of Chinese companies ADS price and cast doubt on their long term performance.

In reaction to this political escalation by congress I only have one option. Which is to liquidate my recently acquired position for a nominal change in value and be done with this affair. I do not like this option because I firmly believe Jinko Solar is well positioned to capitalize on the World’s transition to renewable energy. Their ability to manufacture high efficiency solar panels at extremely low costs represent a competitive moat that is difficult to overcome. Additionally the company is currently the largest manufacturer of pv-modules and would probably extend this lead over time. I also believe their relatively inexpensive panels represents an ability to strengthen margins over time and become increasingly more profitable over the next five years or so. Also by divesting from the actual solar projects themselves and focusing solely on the production of pv-modules they are focused on doing what they do best. It is an unfortunate political escalation which has both dramatically clouded their long term prospects and led to a real reduction in their market value.

Jinko Solar is currently the world’s largest Photovoltaic Module manufacturer. Their current manufacturing capacity of Jinko is roughly 40 GW . This demonstrates tremendous growth from just 8 GW a few years ago. The share price of the company has not reflected this amazing growth in capacity has not been reflected in it’s share price. Additionally, management continues to plan for increasing capacity during the economic downturn. This should demonstrate the resilience of the company. While China, the company’s domestic market, accounts for ~85% of their revenue, the company is expanding into EMEA and America. The potential of these new markets offers tremendous sales and profit growth for the company. A point of concern may be the stated low margin of 3% for the company’s products. However, this margin reflects sales of all the company’s products. Jinko, being a vertically integrated PV-module manufacturer sales many low margin products across it’s value chain. This does not reflect the true margin of close to 18% on the company’s primary offering. Another point of concern may be the heavy debt load of the company. While the debt load is natural for an industrial company of this size, the operating cash flow from the company’s sales is more than enough to cover these debts. The company also said that their customers have not asked for shipment delays during the pandemic.

The reason I believe the market has been so pessimistic towards Jinko Solar, is because the price of Energy is currently so cheap. However, this pessimistic view undermines the potential growth of the sector and the growth of the company’s PV modules sales over time. Also, the company has impressive return on dollars spent on R&D. The current sales of the company come from (I believe not 100% sure) about ~$200 million. These products now sell $6 billion dollars a year. This impressive return on R&D bodes well for the company. For example AMD had been cultivating a line of products with potential growth, however it was only years later these investments began to pay off. A similar story is unfolding here with Jinko.

I began buying Jinko Solar around $15 a share and increased my share as the stock approached $16. I believe these prices represent a significant margin of safety of around ~40%. This substantial margin of safety represents a good investment for the short time and a great investment over a longer time horizon. I believe as governments and energy companies begin expanding their solar projects demand for Jinko’s products will expand with this industry wide demand.

The underlying assumption I made when analyzing Spirit was that it’s true value or prospective value had changed marginally in the pandemic. Warren Buffett’s announcement of selling all airlines lead me to question this belief. Here is a seasoned investor with a time horizon that is quite literally indefinite. If he doesn’t see a quick or inevitable return in demand, clearly something has fundamentally changed in the market. Another critical error in my analysis is ignoring Spirit’s high fixed operating costs. Reading a seeking alpha article that used Delta and United Airlines operating cost to measure what the fixed cost for an airline is, made me realize that although Spirt and Southwest are highly capitalized it will not be enough. There is no way they can be agile and maintain enough liquidity given their business models. Additionally with such a dramatic and sustained drop in demand it will be impossible to be agile and profitable. With this high level of uncertainty I believe there is not, currently, a sufficient margin of error for a purchase to be made.

So what could change that would make me buy Spirit? Firstly some evidence that the depressed demand will not last and high volumes may return within 12 months. It’s key, especially for Spirit, that volume returns within a year. If demand does not return within a year the company will need to issue significant equity financing. This issuance of stock will dilute shareholders’ stakes considerably. The other airlines will have to take this action significantly earlier than Spirit, but even this well capitalized company might need to as well. The macroeconomic trends will also affect Spirit’s equity price considerably over the next few years. If the country enters a prolonged period of slow or negative economic growth it may take more than a decade to recover volume levels.

Given all of this uncertainty there are clearly better areas to deploy capital. JPM and Google are two of the best managed companies and have exceptionally high returns on equity. JPM is consistently averaging 10%, Google is also boasting some of the largest growth and margins. Both of these companies are much more certain and definitely better areas to deploy wealth than airlines currently. However given the fluid nature of the crisis, airline stocks especially Spirit and Southwest warrants a close look if the market becomes extremely pessimistic about their prospects.

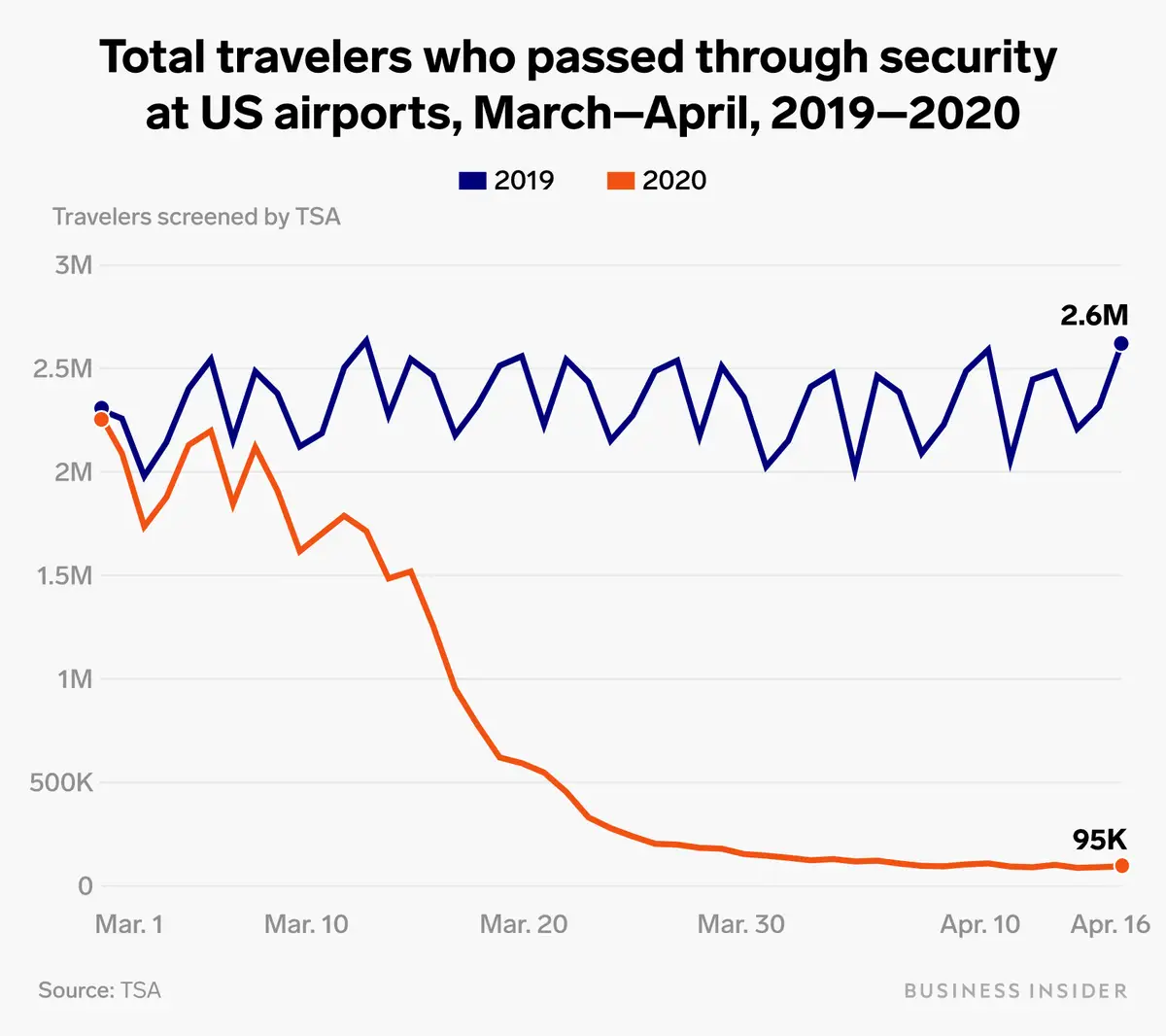

Spirit Airlines will survive the Coronavirus crisis. The company has $894 million in cash and has access to a revolving credit facility of $110 million which carries an interest rate of 2% plus the LIBOR and has the option to increase it to $350 million. Additionally, the company is slated to receive $330 million through the Payroll Protection Program. This means the company should have around $1.2 billion in liquidity with an option to increase it to $1.4 billion. The company’s primary expenses are from labor and fuel which combined account for ~50% of operating costs. The drop in oil prices and reduction in capacity will limit the $1 billion spent on fuel last fiscal year.

Spirit has also cut costs by delaying capital investment and other expenses by $70 – 105 million before any savings from a reduction in capacity. The company has stated that they reduced flight capacity by 80% in April and plan to reduce May capacity by 75%. These reductions should help save a large portion of the $3 billion spent last year on operating costs. Also, all tickets sold by the company are non-refundable, limiting the potential cost of refunding passengers. As long as Spirit can provide transportation, these pre-sold tickets will be recognized as revenue. Assuming a national shutdown does not last for an additional year, the company has adequate liquidity to survive the crisis. Additionally, Spirit is primarily a domestic carrier, meaning border shutdowns do not affect the company as adversely as it does the larger airlines.

Now that the question of survival has been settled, what are the company’s prospects? Currently, at a $13 share price, the company is trading at a price to ‘19 sales ratio of 1:5. Additionally, the company’s market cap is currently below the cash value on its balance sheet. However, the future of Spirit depends on factors largely outside the company’s control. The first question is: When will people fly like normal? The absolute latest time is when a vaccine or effective treatment becomes widely available. The earliest time would be when the U.S. government reduces restrictions and allows carriers to operate normally again and people act indifferent to the pandemic. The timeline on a return to normalcy is probably in the range of 3 – 14 months. With the innate flexibility of Spirit’s corporate structure, the company should be able to significantly cut costs and conserve cash.

However, will air traffic continue to increase after a return to normalcy? Will people be too scared to fly again? People tend to have a very short memory. Now, I’m not an expert in cognitive psychology, but people cannot see the virus. They cannot see buildings crumbling and a crater where one of the world’s tallest buildings used to be. The lack of visceral images renders the virus’s emotional impact less then it might have been otherwise. This leads to a normalcy bias of people minimizing the potential threat to their health and a resumption of pre-Covid behavior. Because of Ultra Low-Cost Carriers (ULCC), like Spirit, there has been continued passenger volume growth over the past decade. While economic downturns tend to decrease total Air demand, ULCCs tend not to be as adversely affected because of their inherent low-cost nature. It does dampen growth by reducing their non-ticket revenue which has become a driver of growth over the past few years. Over the past thirteen years, non-ticket revenue has grown tenfold and represents huge potential for the company. While the growth of this part of the company may stall, it will continue after the crisis and be a principal driver in Spirit’s growth.

The long term prospects of Spirit look bright. Firstly, the company has not been bogged down by the production problems at Boeing, by flying a completely Airbus fleet. The company “operat[es] a single-fleet type of Airbus A320-family aircraft that is one of the youngest and most fuel-efficient in the United States.” This flexibility allows crews to be completely interchangeable and is ruthlessly efficient. Additionally, the company can offer products significantly below the profitable price of other carriers. The largest foreseeable risk is when larger airlines begin offering ULCC rates for a set number of seats in their planes at a loss to take back market share. Such action may adversely affect Spirit’s ability to return outsized gains to its shareholders.

Philip Fischer is regarded as an investing legend and wrote “Common Stocks and Uncommon Profits”. In it, he delineated fourteen points which a company must possess if they will return significant value to shareholders over many years. The points can largely be summarized into four categories: Potential for Sales Growth, Margin growth, Management’s ability, and Labor relations.

The first question that must be asked is, what is Spirit’s potential for Sales growth. According to Statistica the total operating revenue of domestic airlines was $240 billion as of 2018.

Spirit Airlines sales were only $3.4 billion in 2019 and with a potential market of $240 billion, there is significant room for sales growth over the next decade.

The second point to observe is the future of the company’s margin. The current net margin of the company is ~8%. Such a low margin is not enticing, but Walmart and Costco succeed off of low margins with economies of scale and large volumes. As a ULCC Spirit will have low margins initially but will grow as scale is reached and additional passengers serve as pure profit. The ideal future for Spirit would be the American equivalent of Ryanair. Ryanair is a mature European ULCC. Ryanair initially had low net margins but grew them over time as scale was reached. Currently, their net margin is ~ 12% which is 50% higher than Spirit’s current net margin.

Ryanair net margin over time

From both a sales and margin perspective Spirit’s future looks bright. The next two points of discussion are labor and management. Most of Spirit’s workforce is unionized. Additionally, labor accounts for ~30% of operating costs and is extremely important to the Airline business. Adverse labor relations would crimp growth and ruin a potentially great company. However, given the preeminent position labor has in the company’s annual report, it should be safe to assume decent working conditions. Given the company’s low-cost structure pay is below the market average and may not attract the highest quality employees. My personal experience has always been positive when flying on Spirit and always had a positive experience with the employees.

With regards to management the CEO, Ted Christie III, has been with Spirit since 2012. Historically, companies that have promoted insiders to the helm have outperformed their peers that brought in outsiders. Also, the efficiency that Spirit operates with should testify to management’s capabilities.

The market has severely mispriced a growth company at bare bottom prices. Buying Spirit at its current price represents a great investment over the next decade. The company is efficiently managing its resources and has ample opportunity to increase its sales and profitability. The current market is pricing this wonderful company at criminally cheap levels.